2026 Housing Market Outlook – Part II: Inventory, Prices, and Activity Forecasts

Housing Activity Outlook for 2026

Part II of the 2026 Housing Market Outlook focuses on housing activity, not macroeconomic theory. This section breaks down what buyers and sellers should expect in terms of mortgage rates, inventory, home prices, and sales volume as the market continues its transition toward normalization.

Unlike the volatility of recent years, 2026 is shaping up to be a year defined by incremental change rather than extremes. The market is adjusting slowly, creating opportunities for prepared buyers and realistic sellers.

For the full 65 page Compass Intelligence click here or just contact me directly with the request

Mortgage Rate Outlook

Mortgage rates remain the most important variable in the housing market, yet they are also the most difficult to forecast precisely. Historically, mortgage rates tend to fluctuate within a range of roughly 100 basis points each year.

In 2025, mortgage rates traded between approximately 6.1% and 7.2%, with an annual average near 6.7%. For 2026, rates are expected to remain elevated but improve modestly, trading within a projected range of 5.9% to 6.9%, with an average near 6.4%.

Three key forces will influence mortgage rates in 2026:

- A cooling labor market, which typically puts downward pressure on rates

- Narrowing mortgage spreads, allowing rates to decline even if Treasury yields remain elevated

- Persistent inflation risk, limiting how far rates can fall

Mortgage rates are unlikely to return to pandemic-era lows. However, even modest movement toward the lower end of the forecast range could meaningfully increase buyer activity, particularly in higher-priced markets like Orange County.

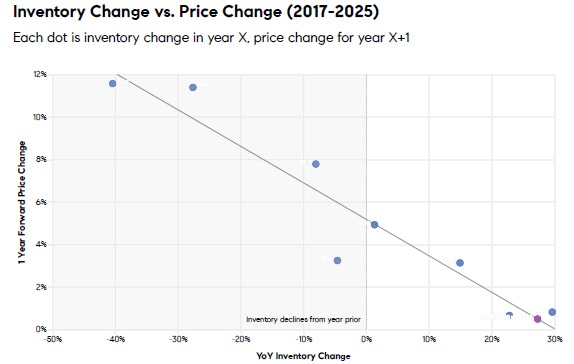

Inventory Outlook: Supply Continues to Rebuild

Inventory growth has been the dominant housing theme of the past several years. Entering 2026, supply remains elevated, but the pace of growth is slowing.

Earlier in 2025, national inventory levels were increasing by 25–35% year over year. By the end of the year, that growth rate slowed to the mid-teens. The base-case forecast for 2026 calls for inventory growth of approximately 10–15%.

Seasonally, national single-family inventory is expected to peak above one million active listings during the summer months before declining toward year-end. By December 2026, total inventory is projected to finish just above 850,000 homes.

This level of supply growth improves buyer choice without creating the type of oversupply that historically leads to steep price declines.

Inventory Risk Scenarios

Inventory levels could exceed forecasts under several scenarios:

- Mortgage rates move unexpectedly higher, reducing buyer demand

- Investor selling accelerates

- Economic conditions weaken meaningfully

Investor-owned properties are particularly important because they add net supply when sold, unlike owner-occupied homes that are typically replaced by another purchase. Rising costs for insurance, taxes, labor, and materials have already compressed investor margins, increasing the likelihood of selective selling.

A sharp deterioration in the labor market could also increase distressed listings, though widespread distress is considered unlikely due to strong homeowner equity positions.

Scenarios Where Inventory Declines

Inventory could tighten if mortgage rates spend sustained time in the mid-5% range while employment remains stable. Under these conditions, buyer demand could absorb available supply more quickly, similar to the brief inventory contraction observed in 2023.

This outcome would require a rare alignment of easing rates, steady job growth, and renewed consumer confidence.

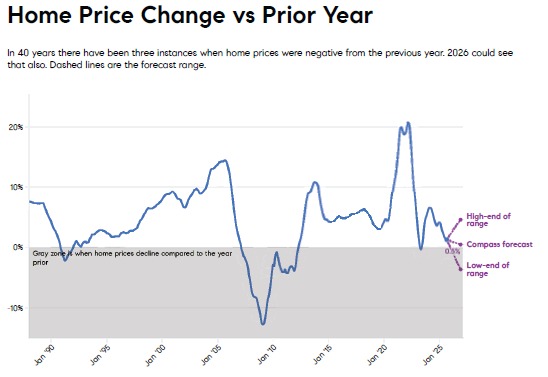

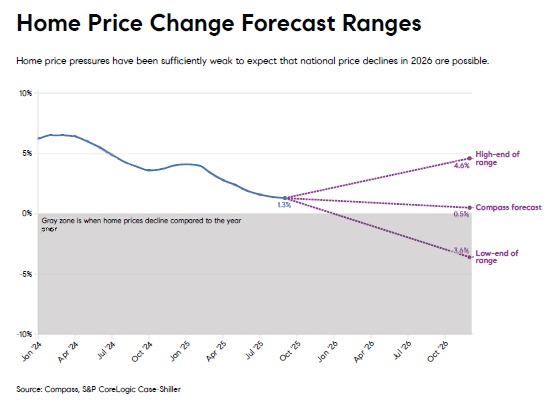

Home Price Outlook for 2026

Home prices enter 2026 under pressure from elevated supply and cautious buyer demand. While national indices continue to show slight year-over-year gains, real-time market data indicates that pricing momentum has largely stalled.

Historically, national home prices have declined in only three periods over the past 40 years. As the market moves through 2026, conditions suggest that another flat year is the most likely outcome.

The baseline forecast calls for approximately 0.5% national price appreciation, with a reasonable range spanning modest declines to modest gains depending on local supply and demand conditions.

Markets with persistently tight inventory are expected to outperform, while markets with large inventory expansions may continue to experience pricing pressure.

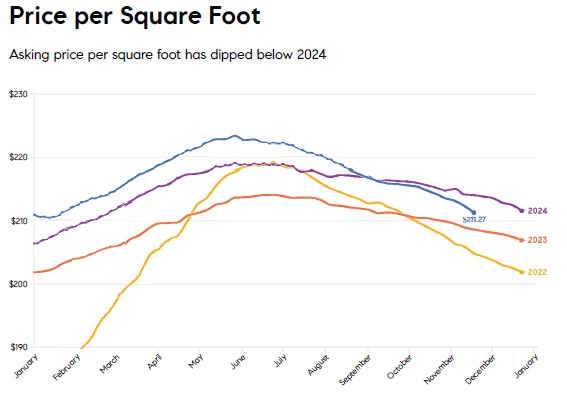

Price Per Square Foot and Seller Behavior

Price-per-square-foot trends often signal market direction before headline price indices. By late 2025, national price-per-square-foot data had slipped below prior-year levels, declining approximately 0.3% to 1% year over year.

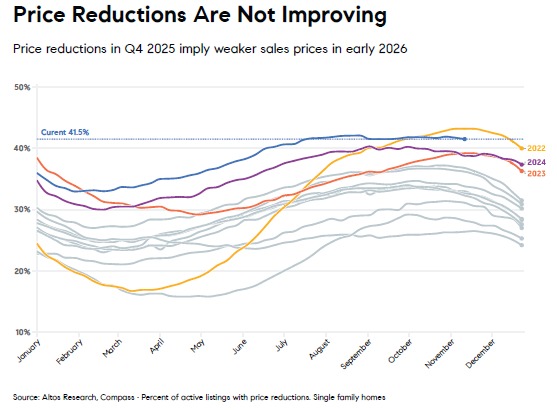

Price reductions further reinforce this shift. Approximately 42% of active listings have taken at least one price cut, one of the highest levels observed in more than a decade. Elevated but stable reduction rates suggest ongoing adjustment rather than market deterioration.

For sellers, this environment rewards realistic initial pricing and strong presentation. Overpricing continues to result in longer market times and multiple reductions.

Sales Volume Outlook

Sales activity is expected to improve modestly in 2026 as affordability stabilizes and inventory continues to rebuild. Nationally, existing home sales are projected to rise approximately 5% year over year.

This increase reflects improved market function rather than speculative demand. As more homeowners become willing to move and buyers regain confidence, transaction volume should gradually normalize.

What This Means for Orange County Buyers and Sellers

For Orange County the 2026 outlook points to a market defined by opportunity and selectivity.

Buyers benefit from increased selection, fewer bidding wars, and improved negotiating leverage. Sellers can still achieve strong outcomes, but success depends on accurate pricing and preparation rather than momentum-driven appreciation.

While Orange County remains more supply-constrained than many U.S. markets, it is not immune to national trends. A flatter pricing environment rewards strategy on both sides of the transaction.

Part II Final Takeaway

The 2026 housing market is transitioning toward balance. Mortgage rates are stabilizing, inventory growth is slowing, prices are flattening, and sales activity is gradually improving.

What This Means Heading Into 2026

For buyers:

Selection should improve modestly

Competition will remain neighborhood-specific

Rate movement matters more than price speculation

For sellers:

Pricing strategy matters more than ever

Overpricing leads to stagnation

Well-positioned homes still transact

2026 will not be a year of extremes, but rather a year where market fundamentals matter again. Buyers and sellers who understand these dynamics will be best positioned to succeed. It’s about function returning to the market.

Want the Orange County–specific takeaway for your neighborhood?

Market conditions vary dramatically by city, price point, and property type. If you want a hyper-local outlook for your part of Orange County, reach out anytime.

For the full Compass Intelligence Outlook for 2026 Housing Market visit.

https://www.compass.com/research/market-outlook/agents/patrick-parry/

Frequently Asked Questions

Nationally, home prices are expected to be mostly flat in 2026. In Orange County, limited inventory and strong homeowner equity should help prevent meaningful price declines.

Mortgage rates are expected to remain in the mid-6% range. Even small dips toward 6% could increase buyer activity in Orange County.

Yes, affordability is slowly improving as prices flatten and incomes rise. In Orange County, improvement will be gradual due to higher home prices.

Yes. Nearly 20% of homeowners now have mortgages above 6%, making them more willing to sell and increasing inventory without distress.

Likely yes. Orange County’s limited supply and high equity levels should support more stable pricing than many U.S. markets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}