2026 Housing Market Outlook (Part 1): A New Era Takes Shape — What It Means for Orange County, CA

The U.S. housing market is quietly turning a corner heading into 2026.

After nearly four years of post-pandemic disruption—volatile mortgage rates, frozen mobility, record affordability pressure, and extreme regional imbalances—the market is no longer operating in “shock mode.” According to the Compass 2026 Housing Market Outlook, we are entering a new housing era defined by normalization, not collapse.

Nationally, prices are flattening, affordability is slowly improving, and transaction activity is beginning to improve. Locally, in Orange County, California, these same forces are playing out inside one of the most supply-constrained, equity-rich housing markets in the country.

This is Part 1 of a multi-part 2026 outlook. Here, we focus on the macro foundation, affordability, mortgage rates, and why Orange County behaves differently than much of the U.S. This is a Summary of the Compass Market Intelligence National Outlook for 2026 and how that compares to the Orange County Housing market.

For the full 65 page Compass Intelligence click here or just contact me directly with the request

A New Housing Market Era Begins in 2026

The key takeaway from the national outlook is simple but important:

2026 is not a crash year. It’s a recalibration year.

Compass forecasts:

National home prices essentially flat in 2026 (forecast +0.5%, with a modest downside and upside range)

Existing home sales rising roughly 5% year over year

Inventory growing about 10% nationally

Mortgage rates largely trading between 5.9% and 6.9%, averaging near 6.4%

This combination would make 2026 one of the rare years since 2010 where price appreciation is minimal, but market function improves. For Orange County buyers and sellers, that distinction matters.

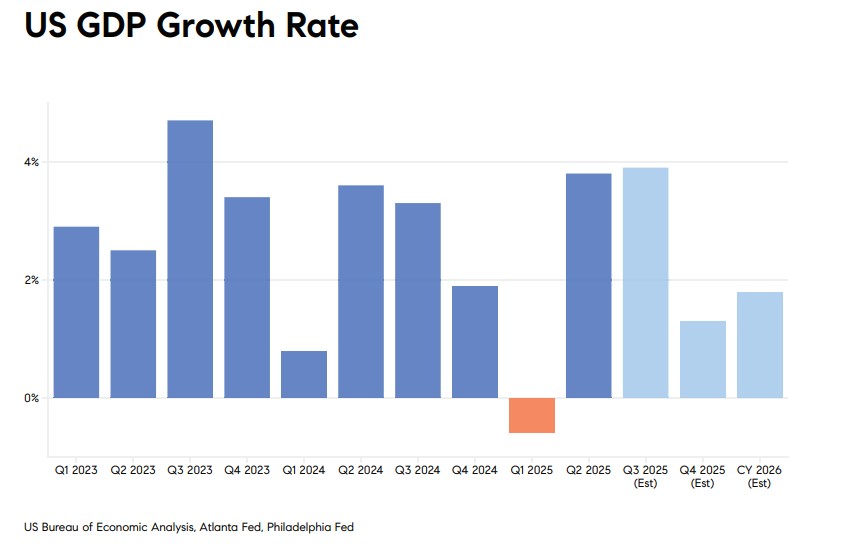

U.S. GDP Growth — Why Housing Has a Floor

Despite years of recession headlines, the broader U.S. economy continues to grow. GDP expanded at a real pace of nearly 4% in mid-2025 and is projected to remain positive into 2026

The economy is best described as K-shaped:

Higher-income, asset-owning households continue to benefit from equity markets and AI-driven growth

Younger and lower-income households face tighter credit, slower hiring, and affordability stress

This matters for housing because it explains why:

Luxury and coastal markets remain resilient

Entry-level affordability remains strained

Forced selling remains limited

In Orange County, where homeowner equity is high and incomes skew above national averages, this economic backdrop provides price support—even in a flat market.

Economic Growth With Real Risks in 2026

Economic forecasters broadly expect U.S. growth to continue into 2026, supported by easing monetary policy, elevated government spending, early-stage AI investment, and unusually strong household balance sheets.

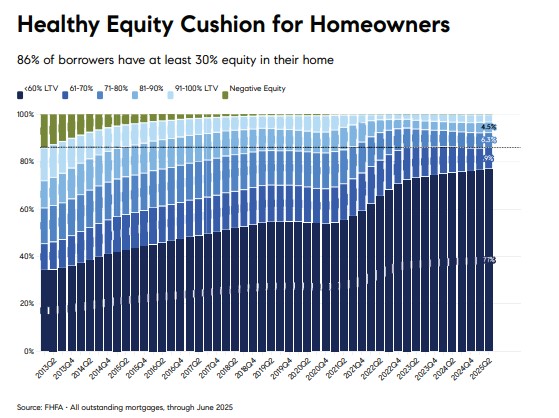

Homeowners enter this cycle with record equity, low delinquency rates, and conservative leverage—key reasons a housing collapse remains unlikely.

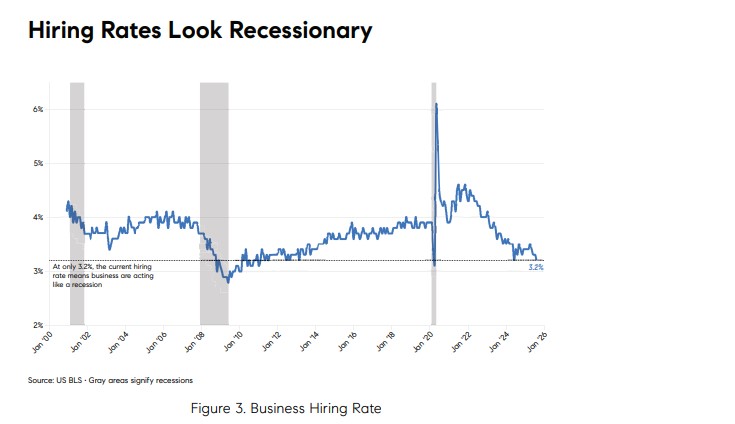

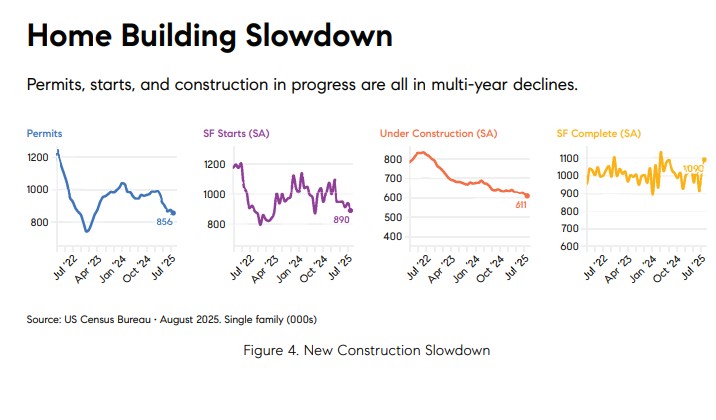

Downside risks remain. Hiring has slowed to recession-like levels, construction activity is down sharply from recent peaks, and consumer sentiment remains weak as costs stay elevated. These pressures matter, but housing downturns typically follow sustained job losses not hiring slowdowns.

For Orange County, this mix points to stability over disruption: slower growth, muted price appreciation, and gradual normalization rather than forced selling and sharp declines.

Improving Affordability — Without a Price Crash

Affordability reached its worst level in nearly 40 years in late 2022. Homes remain roughly 25% above traditionally affordable levels when measured by price-to-income ratios.

But the path back is not a 2008-style correction.

According to the report, affordability improves through:

Flat or slightly softer prices

Rising household incomes (around 4% annually)

Gradually easing mortgage rates over time

The affordability chart shows the price-to-income ratio beginning to trend lower after peaking in 2022. This improvement is slow—but meaningful.

For Orange County, affordability recovery will lag the national average due to higher baseline prices and limited supply. That said, even flat pricing over multiple years materially improves purchasing power when incomes continue rising.

This is especially relevant for:

Condos and townhomes

Inland OC markets

Buyers trading lifestyle flexibility for location value

Mortgage Rates: Why the 6% Threshold Matters So Much

One of the most actionable insights in the report is behavioral—not theoretical.

Buyer activity consistently increases when mortgage rates approach 6%.

Mortgage Rates Over the Past Four Years

Over the past three years, rates have dipped near 6% three times. Each time, buyer demand picked up. At 6.5%–7%, buyers hesitate. At 6.1%, they move

This is not because 6% is “cheap.”

It’s because relative improvement unlocks psychology.

In Orange County, where loan sizes are larger, even small rate changes dramatically impact monthly payments—especially for move-up buyers with equity.

The Mortgage Rate Lock-In Effect Is Finally Fading

For years, homeowners were stuck. Trading a 3% mortgage for a 7% one didn’t pencil, even when life demanded a move.

That dynamic is changing. The longer rates stay elevated, the more homeowners enter the market with higher-rate loans. Those homeowners behave very differently. They’re not anchored to a rate they’ll never see again. They’re more willing to move, more willing to sell. In 2026, roughly 10 million homeowners will have mortgages above 6%, creating a growing pool of potential sellers who won’t feel locked in place.

Expensive vs. Cheap Mortgages

Nearly 20% of outstanding mortgages now carry rates above 6%, and that share continues to grow.

As more homeowners hold “normal” mortgages, they behave differently:

They’re more willing to sell

More willing to move

Less anchored to a once-in-a-lifetime rate

For Orange County, this means inventory can rise modestly without distress, supporting transactions without collapsing prices.

AI, Employment Risk, and the Interest Rate Tradeoff

A growing wildcard for the 2026 housing market is artificial intelligence. While AI investment supports economic growth and equity markets, it is also accelerating job displacement—particularly in white-collar, middle-income roles that historically supported housing demand. This creates a real tension: falling interest rates may improve affordability, but they are likely responding to a weakening labor market, not economic strength.

No housing market is immune to this dynamic. Even in Orange County, where incomes are higher and equity cushions are strong, housing ultimately depends on employment stability. If job losses accelerate, buyer confidence—not rates—becomes the limiting factor.

The key distinction for 2026 will be timing. AI-related job disruption appears gradual, suggesting slower demand growth and cautious buyers. That supports normalization instead of a crash.

Why Orange County Is Different From the National Average

National averages hide local reality.

Many Sun Belt markets are working through excess inventory. Orange County is not.

OC remains defined by:

Structural land constraints

Strong household balance sheets

High equity cushions

Consistent demand for lifestyle, schools, and coastal access

As mobility slowly unlocks and affordability improves at the margins, Orange County is positioned to normalize before it weakens.

In Part 2, We’ll break down what buyers and sellers should expect in terms of mortgage rates, inventory, home prices, and sales volume as the market continues its transition toward normalization.

Want the Orange County–specific takeaway for your neighborhood?

Market conditions vary dramatically by city, price point, and property type. If you want a hyper-local outlook for your part of Orange County, reach out anytime.

For the full Compass Intelligence Outlook for 2026 Housing Market visit.

https://www.compass.com/research/market-outlook/agents/patrick-parry/

For part 2 of the report click here

Frequently Asked Questions

Nationally, home prices are expected to be mostly flat in 2026. In Orange County, limited inventory and strong homeowner equity should help prevent meaningful price declines.

Mortgage rates are expected to remain in the mid-6% range. Even small dips toward 6% could increase buyer activity in Orange County.

Yes, affordability is slowly improving as prices flatten and incomes rise. In Orange County, improvement will be gradual due to higher home prices.

Yes. Nearly 20% of homeowners now have mortgages above 6%, making them more willing to sell and increasing inventory without distress.

Likely yes. Orange County’s limited supply and high equity levels should support more stable pricing than many U.S. markets.

{kind=link}

{kind=link}

{kind=link}